Neobanks are built on latest technology stacks and focus relentlessly on solving specific customer needs.

Prevailing cookie-cutter strategies and monolithic business models limit banks in reaching their full potential. That’s why banks will embrace more diversified strategies that are tailored to meet the needs of specific customer segments.

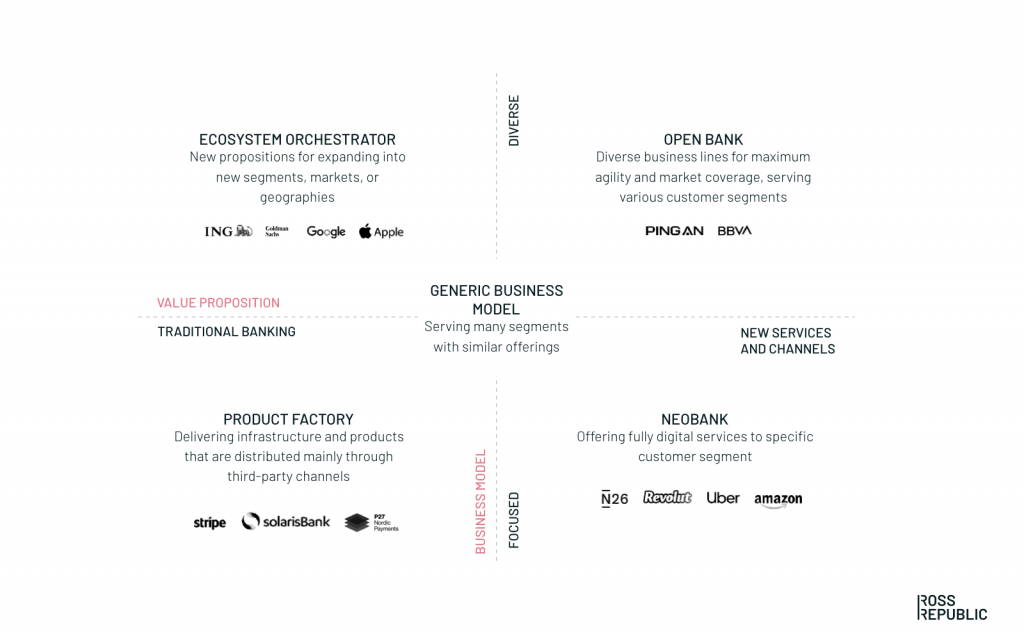

This series of blog posts introduces four strategic archetypes that help banks to win in the digital banking era. The first article of the blog series can be found here.

DIGITAL BANKING ARCHETYPES. SOURCE: ROSS REPUBLIC ANALYSIS

Neobanks provide niche excellence

Neobanks are first-movers that utilise latest technology stacks and set new customer experience benchmarks. That’s why they run on fully digital operations and digital-era business models. A key success factor is the laser-focus on solving key pain points of a customer segment that can be served exceptionally well.

Many consumer-facing neobanks mostly innovate around digital customer journeys and experiences. After un-bundling their incumbent competitors with a vastly improved niche product, they often re-bundle again by complementing their own core features with value-adding third party products (e.g. investing, lending, cross-border payments, insurance, accounting). In most cases, the neobank still controls the end-customer experience.

Revolut is a prime case for a neobank. The UK-based fintech has set a new benchmark for all digital consumer banking players. Further, Revolut partners up with various providers to speed up time to market and to maintain the focus on the core value proposition. In order to launch its account aggregation feature, it partnered with API provider TrueLayer, while Flagstone enables Revolut Metal customers to earn interest on its savings vaults feature.

As banking infrastructure is increasingly provided by whitelabel third parties, many non-financial services companies will become neobanks. For instance, Uber partnered with BBVA in Mexico to allow Uber drivers and their families to create a digital account that is linked to the Driver Partner Debit Card. That’s how Uber is becoming the go-to bank for over 500 000 drivers in Mexico, which can directly receive their earnings within a few minutes.

What does it take to become a neobank?

People and culture: Building a greenfield environment that is free from any traditional legacy organisational structure, process or technology. The culture builds on a customer-centric and agile mind-set, often with autonomous teams that are fully responsible for their specific business line and OKRs (objectives and key results).

Recently, many incumbent banks launched their own neobanks, such as:

- Marcus (Goldman Sachs)

- Mettle (Natwest)

- Bó (RBS)

- Fyrst (Deutsche Bank)

- Azlo (BBVA)

- Openbank (Santander)

In order to attract the right talent, neobanks started by incumbents require full autonomy over their operations and processes. Separate governance as well as budgeting are further success factors.

Business model: The fundamental advantage of neobanks is the low cost-to-serve due to a focus on digital channels and modern IT stacks, which almost eliminate marginal costs of maintaining new customer accounts. Furthermore, neobanks streamline their product portfolio around key customer needs, offer fully digital value propositions, and experiment with new monetisation and digital business models. In contrast to traditional interest-based business models, many consumer-facing neobanks focus on extracting revenue out of their customer base via land-and-expand upsell strategies, recurring revenue through tiered subscription fees, third party commission fees as well as interchange revenue.

Technology: With a strong focus on customer experience design, neobanks often develop proprietary frontend frameworks. Most non-differentiating parts of the business, such as the backend cloud infrastructure, is outsourced to Amazon Web Services (AWS) or Google Cloud Platform (GCP). In order to maintain control over the customer experience, most key features are fully vertically integrated as proprietary in-house solutions. For instance, Monzo developed its own core banking system from scratch, backed by a highly scalable and modular microservices architecture, which is a stark contrast to the prevailing monolithic software packages. Thus, the IT deployed and the level of data utilisation at many neobanks is far ahead of the industry incumbents.

Read next: Product factories provide the infrastructure for open banking

About the author

PARTNER, DIGITAL BANKING

Adrian Klee

Adrian is an expert in building digital business in the financial services sector. He has a background in Fintech and Consulting, and specialises in market research, digital service development and lean venture building.